| |

Summary |

|

| |

|

This briefing outlines the UK pension implications for an employer (Employer) and its parent company (Parent) of:

- a

dividend by the Parent to shareholders; and

- an

intra group dividend by the Employer to its Parent (eg to fund the

Parent to pay its own dividend).

Both the companies and the trustees may need to consider the implications of the payment of such dividends on the security for the pension scheme, in particular whether dividends would mean:

- the existing funding arrangements need revision; or

- the Pensions Regulators moral hazard powers could apply.

Dividends

can affect the strength of the employer support (covenant) available

to a pension scheme. If there is a material adverse change,

the trustee may look at its options to agree new ongoing funding

arrangements. Dividends will also be relevant when trustees

look at the affordability of deficit contributions. A dividend

could also trigger the Pensions Regulator looking to see if

it should use its ‘moral hazard’ powers to issue

a contribution notice or a financial support direction in connection

with (or as a result of) the proposed dividend.

There

are various actions that the Parent and the Employer could undertake

to limit any Trustee concerns regarding the impact of the proposed

dividend on the Scheme.

The

potential disclosure obligations in relation to a proposed dividend

also need to be considered. |

| |

Pensions issues on proposed dividends |

|

| |

|

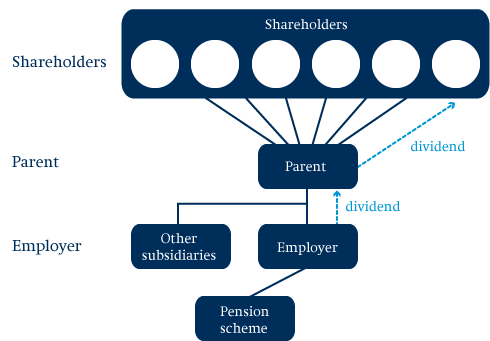

Companies will often want to pay dividends to shareholders whether:

- by a parent company out of the group (to ultimate shareholders); or

- within a group, from (say) the employer to the (non-employer) parent company.

A (simple) example is:

Pension

schemes are direct creditors of the relevant Employer (by reason of the

statutory funding obligations under the Pensions Act 2004 and the debt

on employer provisions in section 75 of the Pensions Act 1995). Schemes

are not automatically direct creditors of other companies in the group

(absent a direct guarantee or the Pensions Regulator exercising its moral

hazard powers) – see our briefing No 220, Pension

debts – priority

of claims.

Dividends can affect the strength of the support (covenant) available to a pension scheme. Proposed dividends raise three main pensions issues:

- does any change in the strength of the covenant impact on ongoing funding arrangements?

- does any dividend raise potential risks of the Pensions Regulator exercising its moral hazard powers?

- what are the disclosure and notification obligations? How is any conflict of interest dealt with?

Trustee and funding

The

effect of a dividend is that the Employer may need to agree new ongoing

funding arrangements with the trustee of the Scheme (the Trustee). The

Trustee is likely to take a dividend into account when assessing the

strength of the Employer as the principal employer of the Scheme, and

any additional support that could be expected from the Parent. The effect

of:

- a dividend from the Employer to the Parent, is to weaken the strength of the Employer, but this may be counterbalanced (to a degree) by the extra strength given to the Parent (depending on what the Parent plans to do with the proceeds of the dividend and the degree of support that the Trustee sees from the Parent as part of the Employers wider group).

- dividend from the Parent to its shareholders, is to weaken the strength

of the Parent. The materiality of that to the Scheme will depend on

the size of the dividend and the degree of support that the Trustee

sees from the Parent as part of the Employers wider group’ (as

opposed to the shareholders who may not be).

Depending

on size and materiality, the dividend can affect the level of contributions

which the Trustee seeks from the Employer (see ‘Funding implications’

below).

See

the section on ‘Funding implications’ below.

Potential moral hazard risk

The

Pensions Regulator (TPR)

could in some circumstances use its moral hazard powers1 to

issue a contribution notice (CN)

or a financial support direction (FSD) in connection

with (or as a result of) the proposed dividend.

In order to issue a CN or an FSD against someone that is not a participating employer of the Scheme:

- that

third party must be ‘connected’ or ‘associated’ with

a participating employer;

- the relevant conditions for issuing a CN or an FSD must be met; and

- TPR must consider it reasonable to issue such a notice.

The

following entities/persons, in particular, are connected or

associated and so could be potential targets for TPR’s

moral hazard powers:

- parent and other entities in the Parent group; and

- the directors of the Employer.

See

the section on ‘Moral Hazard Powers’ below.

Disclosure/Conflicts of Interest

The

Employer and the individual directors of the Trustee board have

certain duties to disclose information to the Trustee board. See

the section on ‘Disclosure’ below. |

| |

Limiting the Trustees concerns |

|

| |

|

The Parent and the Employer could undertake the following actions to limit any Trustee concerns regarding the impact of the proposed dividend on the Scheme:

Explain the groups dividend policy to the Trustee

This action does not seek Trustee consent, but merely clarification that the Trustee board is aware of the position. This may also allow the company to claim that dividends are not material (either for moral hazard purposes or scheme funding). It also reduces the potential for the Trustee seeking changes to the current ongoing funding arrangements.

However, it must be remembered that this offers no express clearance or exemption from moral hazard powers.

Agree the dividend with the Trustee

The dividend policy of the Employer/Parent could be agreed with the Trustee, at the time or in advance (eg as part of the scheme funding negotiations). This should allow the company to claim that dividends within that policy are not material (either for moral hazard purposes or scheme funding).

Mitigate any reduction in the Employer covenant

In relation to a material dividend from the employer to the parent, mitigation could be offered eg a parent company guarantee may result in no overall covenant reduction (and could improve the schemes PPF levy situation), but would also formally tie the Parent to the Employer and Scheme. Furthermore, a parent company guarantee would not then be available for future negotiations if needed.

Seek clearance from TPR

Formal clearance from TPR will provide comfort to the parties on TPRs moral hazard powers (but only to the extent of the facts as disclosed). TPR or the Trustee may also want extra funding in return and the clearance may not cover all future events. |

| |

Funding implications |

|

| |

| As part of the scheme specific funding arrangements (under the Pensions Act 2004), the Trustee will need to consider the strength of the employer covenant supporting the plans when assessing scheme specific funding. Trustees increasingly look for a formal covenant review and the proposed dividend will be relevant to this assessment.

Dividend from the Employer

An

intra-group dividend from the Employer to the Parent would have the effect

of reducing the net assets of the Employer. The Scheme would usually be

(eg if an insolvency occurred) an unsecured creditor of the Employer.

Depending on the financial impact, the Trustee may consider a dividend

to be a material change when looking at covenant issues. This will have

an effect on the negotiation of future funding.

The impact of this may in some cases be reduced, given that the Parent is part of the Employers wider group and so may (depending on the circumstances) be an entity that the Trustee may look to for support in any event.

Dividend from the Parent

As

stated above, schemes are not automatically direct creditors of other

companies in the group (absent a direct guarantee or the Pensions Regulator

exercising its moral hazard powers)2. But schemes may have

an interest in the strength of the Parent for various reasons:

- the

Employer may be a creditor of the Parent (eg if it has lent funds to

the Parent). So the strength of the Employer depends (in part) on the

ability of the Parent to repay that debt;

- the

Parent may have given security or support direct to the Scheme; or

- the

Scheme may consider that TPR could exercise its moral hazard powers

(see below) and force the Parent to contribute or give security to

the Scheme; and

- the

Parent will form part of the wider group3 on which

the Employer or the Scheme may be able to rely (to a degree) in

practice even absent a formal legal obligation.

What can the Trustee do?

The Trustees powers, when faced with a dividend (or notice of a potential dividend), to raise employer contributions, depend on the terms of the scheme and the funding arrangements already agreed.

- some schemes give the Trustee a unilateral power to fix contributions in such cases, where the dividend has a potentially material impact, the Trustee may consider exercising that power and raising contributions.

- In

other schemes, the rules provide for contributions to be fixed by

the employer or by agreement here the Trustee does not have a unilateral

power to increase contributions, but it may be able to seek agreement

with the Employer on a revision to the funding arrangements in light

of the dividend. The scheme specific funding provisions under the

Pensions Act 2004 include provision for a schemes recovery plan to

be reviewed and if necessary revised where the trustees consider

that there are reasons that may justify a variation to it4.

If the Trustee and the Employer do not agree, then the Pensions Regulator

may have power to impose a new schedule of contributions (s231, Pensions

Act 2004).

TPRs views on dividends

TPRs guidance on Monitoring employer support suggests that trustees and employers should consider increasing scheme security by using contingent assets, including:

negative pledges, whereby an employer makes a commitment not to do something such as grant new security without the agreement of trustees or not to increase dividends.

TPR’s

statements on funding indicate that it expects the funding of

the pension scheme to be taken into account by companies, when looking

at dividend policy. It discourages increases in dividend payments

at a time when recovery plan periods may be looking to be extended.

Its general guidance is for trustees to look for contributions based

on the amount that companies can reasonably afford5. |

| |

| TPR Statement (April 2012)

Pension scheme funding in the current environment (April 2012)

24. Where deficits have increased, some employers will be in a position to accommodate deficit repair contribution increases in their business plans. Others will have significant competing demands making cash contribution increases difficult. Servicing of other debts and facilitation of appropriate capital expenditure are necessary features of successful businesses as part of ensuring ongoing employer support.

25. The pension scheme should, however, be equitably treated among the competing demands on an employer (eg to balance the business dynamics for capital investment and dividends payments with obligations to service debt). Where cash is being used within the business at the expense of what otherwise would have been affordable pension contributions, it is important that it is being used to improve the employers covenant rather than benefits accruing disproportionately to other stakeholders.

26. Most employers can afford appropriate dividend payments without prejudice to the funding of the pension scheme. However, if there is substantial risk to the likelihood of the pension scheme delivering the benefit entitlements promised within it, then dividend payments need to be re-assessed in light of the obligations to the pension scheme, and other creditors.

27. Where the employers covenant has weakened and it cannot afford to continue contributions at previously agreed levels, or is unable to pay more in respect of a larger deficit, trustees may need to agree to a longer recovery plan. A material extension to the recovery plan end date will require sound justification. |

|

| |

Moral Hazard Powers |

|

| |

| The moral hazard powers of TPR include powers to make third parties liable for pension deficits/funding etc in certain circumstances. Such third parties must be connected or associated with an employer, the relevant conditions for issues or issue of an FSD or CN must be met and TPR must consider issue of such a notice to be reasonable.

A dividend has two potential impacts on the risk of a CN or FSD:

- the dividend could itself be a trigger for a CN as being an act that supports a CN; or

- in

the case of a dividend payable to the Parent, the fact of the dividend

having been paid, reinforces the connection of the Parent with the

Employer. It is an example of the Parent having drawn a benefit from

the Employer and so could make it more reasonable to make a CN or

FSD against the Parent. See for example the reasons given by the determinations

panel of TPR in the Box Clever determination in 20116.

|

| |

CNs |

|

| |

| TPR has the power to issue a CN where either:

- a

person has been a party to an act/omission since April 2004, the main

purpose of which or one of the main purposes of which was to avoid

or reduce the s75 pension liability7; or

- an act/failure to act since April 2008 has detrimentally affected in a material way the likelihood of accrued scheme benefits being received.

In both cases TPR must consider it reasonable to issue a CN having regard to factors set out in the legislation.

A

CN can be issued on a person who is (or has been) connected or associated

with the employer8 – eg an individual (eg a director

of the Employer) or a company (eg Parent) who was a party to (or knowingly

assisted) in the relevant act or omission. The warning notice

needs to be issued within six years of the relevant act or omission. |

| |

FSDs |

|

| |

| The primary test for an FSD is financial is the employer a service company or insufficiently resourced? An FSD cannot be made against an individual (where the employer is a company).

Who is potentially liable?

An

FSD in a group situation can only be issued against other group companies.

It cannot be issued against individuals. CNs can be issued against connected

companies (eg Parent) but also against individuals who are associated

or connected with an Employer (eg directors or employees of the Employer9).

They need to be party to (including those who knowingly assist) the

relevant act or omission that triggers the CN.

There is a statutory defence (s38B, Pensions Act 2004) available to the materially detrimental CN test – where a target (eg a director):

- gave due consideration to how the scheme might detrimentally be affected; and

- took all reasonable steps to minimise any detriment; and

- reasonably concluded that the act or failure would not detrimentally affect in a material way the likelihood of accrued scheme benefits being received.

|

| |

Disclosure/Conflicts of Interest |

|

| |

There may be two potential disclosures which arise in relation to a proposed dividend:

- disclosure by the Employer (or Parent) to the Trustee; and

- disclosure by individual members of the Trustee board (who may hold senior positions in the Parent) to the Trustee board.

Employer disclosure/discussion

One issue for the Employer is when to discuss the proposed dividend with the Trustee.

Partly

this depends on whether there is any formal disclosure protocol

that has already been agreed. There is a statutory obligation on

an employer to disclose material events to trustees within one month

of them happening. In addition, an employer is required to disclose

material information if requested by the Trustee (Reg 6, Scheme

Administration Regulations 1996).

There is no obligation to inform the Pensions Regulator about a dividend – dividends are not within the notifiable event obligations10.

Trustee disclosure

The

position where a member of the Trustee board is aware of a proposed

dividend (eg by virtue of his position within the Employer or Parent)

depends on the materiality of the proposal and on the disclosure/conflicts

provisions of the Scheme (or the articles of association of the

trustee company).

The conflicts policy that has been adopted by the Trustee (following the Companies Act 2006 and TPR guidance on conflicts at about the same time) needs to be considered. |

| |

|

|

For

more information please contact |

|

David Pollard |

| T +44 20 7832 7060 |

|

E david.pollard@freshfields.com |

| |

|

Charles Magoffin |

| T +44 20 7785 5468 |

|

E charles.magoffin@freshfields.com |

| Dawn Heath |

T +44 20 7427 3220 |

E dawn.heath@freshfields.com |

Andrew Murphy |

T +44 20 7785 2708 |

E andrew.murphy@freshfields.com |

Alex Fricke |

T +44 20 7785 2282 |

E alexandra.fricke@freshfields.com |

Alison Chung |

T +44 20 7785 2253 |

E alison.chung@freshfields.com |

Harriet Sayer |

T +44 20 7785 2906 |

E harriet.sayer@freshfields.com |

| |

| |